You cannot blame the customer service representative’s. They doing their job and are following company guidelines setout by those above and are told very little of what really is going on or what mbo’s plans are.

https://www.motabilityoperations.co.uk/ you need to look at not https://www.motability.co.uk/ for the true agenda at play.

When we spoke about me leaving the scheme and my many reason’s for doing so, he said he agreed with pretty much all of them personally and understood exactly why and was valid and that they had many calls regarding the same issues I had highlighted.

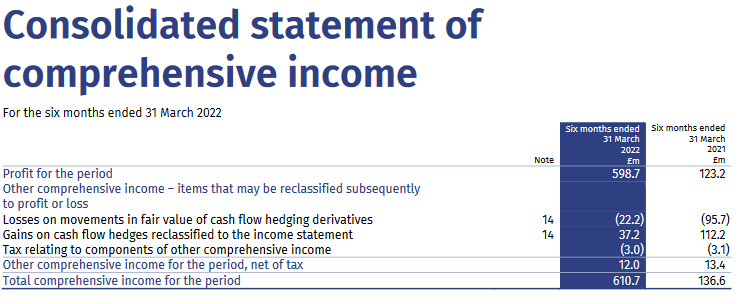

Yet what is MBO doing about it. Offering a £250 otp if and when you get a new car on the scheme, even if that is taken up by the 600k users of the scheme. Thats £150,000,000 but in reality a small percentage of there overall profits even in the past 6 months https://www.motabilityoperations.co.uk/our-performance/financial-reports/ Half year highlights 2022 £598.7m profit / £3,480.1mCapital Reserves as at 31st March 2022 /90%Renewal rate at end of lease. I predit this next 6 months profits will be even larger.

<p style=”text-align: center;”> Notwithstanding a lower volume of vehicles

Notwithstanding a lower volume of vehicles

sold – down 30,000 units compared with 2021

(a consequence of an increasing volume of

lease extensions for existing customers

pending the delivery of their new vehicles)

the proceeds from the disposal of operating

lease assets saw a 8.4% increase in the six

months to March 2022 compared with prior

year, reflecting the elevated sales values

achieved in the used-car market</p>

<p style=”text-align: center;”>Profit for the period was £598.7m, representing

a 10.3% return on assets (above our long-term

target of 1.5%). This above target result is

primarily driven by two effects:

• A gain of £403.9m from vehicle sales (2021:

£78.4m), reflecting the buoyant used-car

market referenced above. The strength of

the used-car market can be directly linked

to the new-vehicle supply-side challenges

faced globally. This has resulted in significant

switching of demand to used cars. Our vehicle

remarketing operation has been able to

effectively capitalise on the conducive

demand conditions in the used-car market,

with average sales values of £15.5k (up 50%)

on prior year not only driving increased

revenue, but leading to crystallised profits

versus the net book value. Whilst this upside

is in part a result of used-car values

exceeding our previous forecast expectations</p>

I got a new vehicle in 4 weeks off the scheme. Not in months and months time or even a year/s which if your car has become unsuitable for reason’s beyond your control, what can the scheme offer you.

I also terminated early, I also mentioned the huge unaffordable ap’s and the lack of choice with only just over 500 cars on the scheme a 1/4 of what was available in the past and that many was just different variants of the same make & model. I don’t see anything changing in the market and many say this is the new normal for the car industry and they’re not going back to how it was before, even with reduced supply they are making huge profits as are MBO from used car sales and those extending lease as in the 2022 report. The next report I think will be even more profits and those profits are not really being given back into the schem all they give are token gesture’s and as we move towrds 2030 it will only get worse for those on the scheme especially if you have no off road parking and those that cannot afford such high ap’s but do not qualify for a grant. Things need to change and be looked into these are huge sums and even bonds.

<p style=”text-align: center;”>The Group continues to pursue a strategy aimed

at diversifying sources of funding, protecting

structural liquidity and maintaining a well-

laddered debt maturity profile. Following the

issue of inaugural bonds under our social bond

framework in January 2021, the Group raised

incremental financing in January 2022 via a

£500m 20-year GBP bond. This bond provides us

with strong liquidity headroom as we look

ahead and in the context of the repayment of a

£400m bond liability due in July 2022.</p>

<p style=”text-align: center;”>Of the Group’s £1,093.8m cash and cash

equivalents balance reported at 31 March 2022

(March 2021: £437.8m), £83.1m is ring-fenced

(March 2021: £149.5m) in respect of insurance

liabilities in MO Reinsurance Ltd. The Group

retains a £1.5bn Revolving Credit Facility to

provide liquidity headroom which was

undrawn at 31 March 2022. Our corporate

credit ratings (A1/A, both with a Stable

outlook; S&P and Moody’s respectively)

remain an important enabler of our access

to financing at competitive rates from the

debt capital markets.</p>

So someone is making and taking profits from the scheme. That is clear as to how much that is unclear as is alot of the accounts it’s just generic and list of a breakdown of the actual cost and items related to those cost of running the scheme. even if there small percertages of huge amounts we talking that’s alot of money, leaving the scheme and not put back directly into the scheme. just had to post this and get it out there.